What They Say About Us

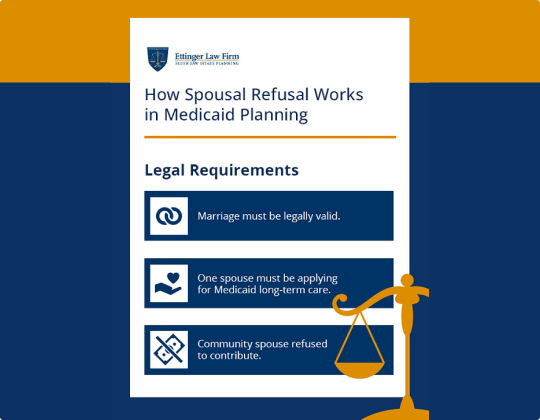

When one spouse needs long-term care, such as nursing home care, they can apply for Medicaid. While Medicaid normally considers both spouses’ income and assets when determining eligibility, under New York law, the “community spouse” who remains at home has the right to refuse to contribute to these care costs. Generally, they may keep $3,948 per month of the couple’s income and an additional $157,920 in assets or resources. Other exempt assets, such as a home and one automobile, are excluded. The spouse being cared for in a facility is known as the “institutionalized spouse.”